De Grauwe, P. (2014) “Stop Structural Reforms and Start Public Investment in Europe“, Social Europe Journal, 17 Σεπτεμβρίου.

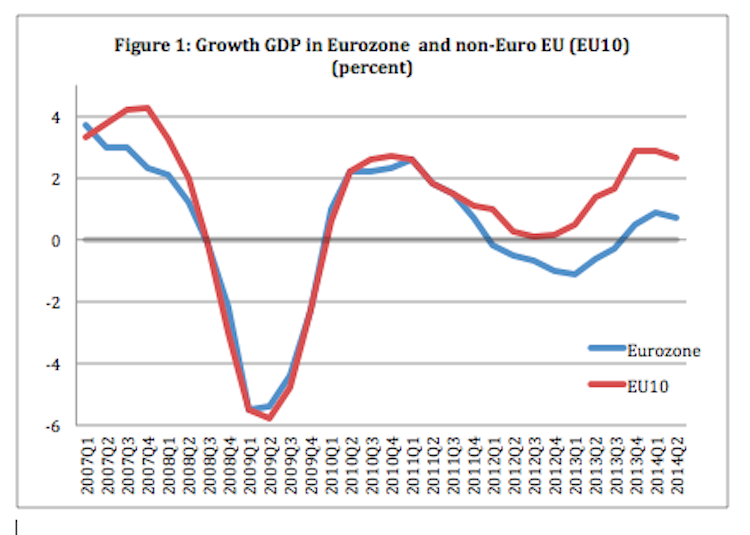

Slow growth in the Eurozone has become endemic since the start of the sovereign debt crisis in 2010. This is made very clear in Figure 1, which contrasts the growth experience of the Eurozone with the non-Eurozone EU-member countries since the start of the financial crisis in 2007. What is striking is that up to the Eurozone sovereign debt crisis of 2010 the growth experiences of the Eurozone and non-Eurozone countries in the EU were very similar. Both groups of countries saw their boom collapse and turn into a deep recession in 2008-09. Both recovered relatively quickly in 2010. Since 2011, however, the two groups of countries depart. The Eurozone experienced a new recession and since then has experienced a growth rate that on average has been 2% below the growth rate of the EU-countries that are not part of the Eurozone.

Πηγή: Eurostat

What happened since the start of the sovereign debt crisis that has led to a systematic decline of economic growth in the Eurozone as compared to the non-Euro EU-members?

In Brussels, Frankfurt and Berlin it is popular to say that this low growth performance of the Eurozone is due to structural rigidities. In other words, the low growth of the Eurozone is a supply side problem. Make the supply more flexible (e.g. lower minimum wages, less unemployment benefits, easier firing of workers) and growth will accelerate.

This diagnosis of the Eurozone growth problem does not make sense. As is made clear from Figure 1 the Eurozone countries recovered as quickly from the recession of 2008-09 as the non-euro countries. If the problem was a structural one, it also existed in 2008-09. Yet these structural rigidities did not prevent the Eurozone countries from recovering quickly in 2010. Why then did structural rigidities from 2011 on suddenly pop-up to produce lower growth in the Eurozone than in non-euro EU-countries, while they did not play a role in 2010? Although this supply-side story does not hold water, it continues to provide the intellectual underpinnings of the Eurozone policymakers who continue to insist on structural reforms.

Σχετικές αναρτήσεις:

- Derviş, Κ. & Saraceno, F. (2014) “An Investment New Deal for Europe“, Brookings Blog, 03 Σεπτεμβρίου.

- Pisani-Ferry, J. (2014) “Can Investment Save Europe?“, Project Syndicate, 30 Ιουλίου.

- Wolff, B. G. (2014) “Europe needs new investment, not new rules – the EU must avoid another useless fight over its fiscal rules and instead use political capital to foster growth“, Bruegel Institute, 25 Ιουνίου.