Monokroussos, P. (2014) “Greek GDP Nowcasting Model Update – Real GDP estimated to have increased by around 1.0% YoY in Q3 2014 (ESA95 terms); first positive annual growth reading since mid-2008“, Eurobank Global Market Research, Greece Macro Monitor, 22 October.

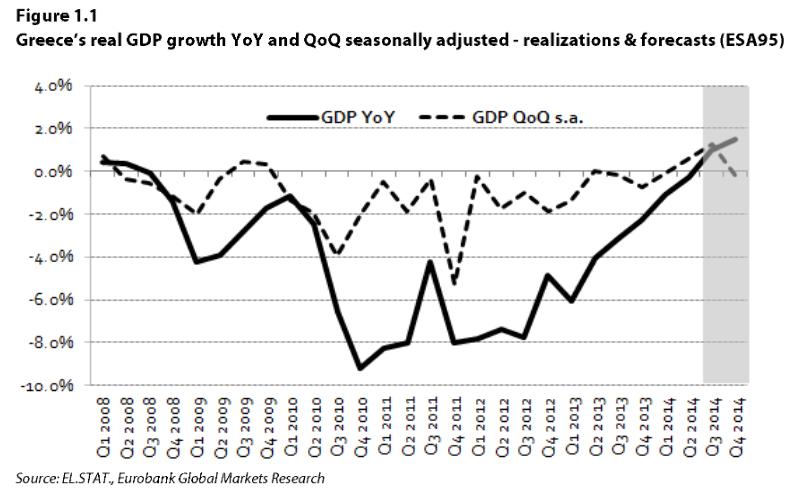

This note presents a preliminary estimate of Greek GDP for the third quarter of this year, based on a range of monthly data released up to October 17, 2014. Our Nowcasting model produces high frequency, real-time estimates of Greece’s gross domestic product by applying an econometric methodology that can properly handle data reporting lags, revisions and other important aspects characterizing the daily flow of macroeconomic information. Our mid-point estimate of real output growth in Q3 is for a switch into a positive territory, to c. 1.0% ΥοΥ, from -0.3%YoY in Q2 and -1.1%YoY in the first quarter of 2014. As we explain in the present document, the flow of macro data pertaining to Q3 2014 will continue in the following couple of months. Moreover, Greece’s stats agency (EL.STAT.) is due to release on November 14 new quarterly GDP series, following the recent publication of revised annual data for national accounts pertaining to the period 1995-2013. These revisions integrate new and updated data from various sources. They also reflect the transposition of Greek data into the European System of National and Regional Accounts (ESA2010) that has replaced ESA95. Taking into account the aforementioned developments, our GDP estimate for Q3 2014 should be considered as strictly preliminary and subject to revisions. We will update our analysis following the publication of the revised quarterly series but, for the time being, we maintain our earlier forecast of slightly positive GDP growth for the full year. On a less constructive note, domestic economic activity in the current (4th) quarter is likely to face a number of headwinds, including a worsening stream of macroeconomic data from the euro area and prevailing domestic political uncertainty ahead of the presidential election.